Updated September 2023

People who enroll in coverage through a health insurance marketplace must pay a monthly premium in order to effectuate and maintain their coverage. The following FAQ explains marketplace policies on premium payments, grace periods for people who do not pay premiums on time, and termination of coverage for failure to pay premium amounts owed at the end of a grace period.

What is a premium?

A premium is the monthly charge that an individual must pay for health insurance coverage. Individuals must continue paying the premium for each month they are enrolled in a health plan until they cancel or change their plan, or else their coverage will be terminated.

When are premiums due?

Premium payments are generally due around the beginning of the month of coverage. For example, the premium for May might be due on May 1 or April 30. The exact due date of the premium may vary from state to state and among insurance companies. The insurance company will send a bill each month indicating the amount of the premium that is owed and when it is due.

When must the premium for the first month of coverage be paid?

Individuals who select a qualified health plan (QHP) in the marketplace must pay the first month’s premium to complete the enrollment process. This is sometimes called the “binder payment.” A person who applies for coverage and selects a plan, but then fails to pay the first month’s premium, will not be enrolled.

In the Federally-Facilitated Marketplace (FFM), the first month’s premium is due on the effective date of coverage for coverage that begins prospectively (e.g., May 1 for coverage that starts in May). Insurers can choose to set the due date for the first month’s premium up to 30 days after the effective date of coverage. Subsequent months may have a different due date for the premium payments.

For some special enrollment periods (SEPs), coverage can begin retroactively. For people who qualify for these SEPs, insurers must set the deadline for the first month’s premium payment deadline at least 30 days after plan selection. For coverage to begin retroactively, an individual must additionally pay premiums for all months of retroactive coverage by this deadline. If the person only pays the premium for one month of coverage, their coverage will begin on the first day of the month following plan selection.

State-based Marketplaces (SBMs) can establish their own policies for the due date of the first month’s premium, or they can implement the FFM’s policy.

If a person fails to pay the first month’s premium but is still in an open enrollment or special enrollment period, then the individual may go back to the marketplace and reselect a plan. If the non-payment occurs after the open or special enrollment period has ended, the individual will not be able to enroll again, and will have to wait until the next open enrollment period (unless they qualify for a special enrollment period at some point during the year) to re-enroll. For example:

- John applies for coverage during open enrollment between November 1, 2023 and January 31, 2024 and selects a plan on January 10, 2024, with a coverage effective date of February 1, 2024. However, he fails to send in the February premium by the February 1 due date. Therefore, he is never enrolled in the plan, and he cannot enroll until the next open enrollment period in the fall of 2024 unless he qualifies for a special enrollment period before then.

- If instead he selects a plan on December 10, 2023 with a coverage effective date of January 1, 2024, and fails to pay the January premium by the January 1 due date, he is never enrolled in the plan, but because the open enrollment period has not ended, John can go back to the marketplace and select a plan (with a February 1 effective date) before the end of open enrollment on January 15, 2024.

How are premiums paid?

Individuals purchasing coverage through a marketplace can pay their premium directly to the insurance company. The marketplace in some states may also allow enrollees to pay the premium to the marketplace, which will then transfer the payment to the insurer(s).

All plans sold in the marketplaces are required to offer consumers at least the following payment methods:

- check;

- money order;

- general purpose pre-paid debit card; and

- Electronic Fund Transfer (EFT).

Some states may require insurers to offer additional payment methods, such as credit card, debit card, or cash. Insurers can also voluntarily accept these additional payment methods even if they are not required to do so.

What happens if a premium is not paid on time?

Enrollees who fail to pay their premium by the assigned due date have a grace period before their coverage can be terminated. The grace period is different for enrollees who receive an advance premium tax credit (APTC) and those who do not. Enrollees receiving an APTC have a grace period of three months. Those who do not receive an APTC have a grace period that is set by state law or regulations (generally 30 or 31 days, or left to the insurer’s discretion).

Enrollees in a grace period can maintain their coverage if they pay all outstanding amounts owed to the insurance company before the grace period ends. A partial payment will not change the end date of the grace period. If they fail to pay the amounts they owe, the insurer can terminate their coverage. The examples in Figure 1 illustrate how the grace period works:

- Jane receives an APTC and fails to make her April premium payment by the required due date. She is in a 3-month grace period that expires on the last day of June. The premium for each month of the grace period is added to the amount owed. To return to good standing by the start of May, Jane would have to pay the premiums owed for both April and May. To be in good standing by the start of June, she would have to pay the premiums owed for April, May, and June. To avoid plan termination when her grace period ends at the end of June, she would have to pay the premiums owed for April, May, June, and July. If she pays an amount less that the total amount owed during the grace period, she will risk having her coverage terminated if she does not pay the remaining balance by the appropriate due date. If she returns to good standing in May or June, but then misses a future payment, a subsequent grace period is triggered.

- John does not receive an APTC and fails to make his April premium payment by the required due date and enters a grace period that is defined by state law or regulations (in this case, we use one month). If he does not make full payment for both the April and May premiums by the end of the grace period (the end of April), the insurer can terminate his coverage. However, if he pays the required amounts before the end of April, his coverage continues.

| FIGURE 1: How do Advance Premium Tax Credits Affect Grace Periods? |

| JANE: Receives APTCs and is eligible for a three month grace period |

Jane fails to make her April premium payment by the end of March. She enters a 3 month grace period. |

| JOHN: Does not receive APTCs and is eligible for a one month grace period |

John fails to make his April premium payment by the end of March. He enters a one month grace period. |

Does someone who is eligible for a premium tax credit but elects not to receive the credit in advance qualify for the three month grace period?

No, the three month grace period applies only to people who are receiving an APTC. A person who is eligible for an APTC but elects to wait and claim the premium tax credit when they file their taxes will only qualify for a grace period that is set by state law or regulations, which is generally 30 or 31 days or left to the insurer’s discretion.

If a person re-enrolls in a marketplace plan during open enrollment, do they need to pay the first month’s premium for the new plan for coverage to begin, or will they be eligible for a grace period?

If a person fails to pay the first month’s premium after being automatically re-enrolled in a health plan in the FFM, they will enter into a grace period. However, if a person who was previously enrolled in a QHP actively enrolls in the same plan or a different plan, they will be required to pay the first month’s premium for the new plan in order for coverage to begin. For example:

- Jane signs up for a QHP beginning in 2023, and is automatically re-enrolled in a similar plan for 2024. She fails to pay her January premium by the January 1 due date. Because Jane has been automatically re-enrolled, she will be eligible for a grace period.

- John signs up for a QHP beginning in 2023. For 2024, he selects a different QHP. He fails to pay his premium by the January 1 due date. Because John has actively enrolled in coverage for 2024, his coverage will not begin on January 1.

What happens if all outstanding premium payments are not made before the end of the grace period?

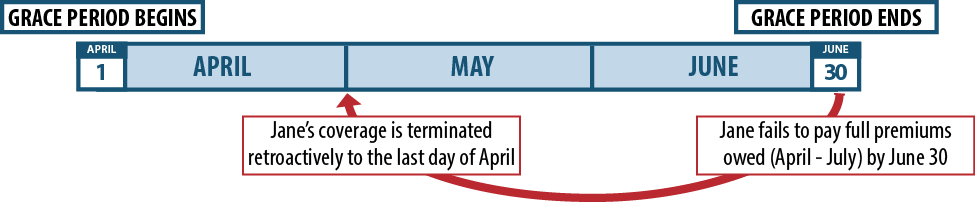

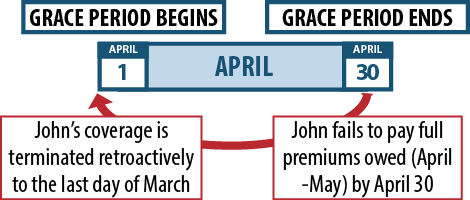

If an enrollee does not pay all outstanding premium amounts they owe by the end of the grace period, their coverage can be terminated. For people receiving an APTC the coverage termination effective date is the last day of the first month of the grace period. For individuals not receiving an APTC, the effective date of termination depends on state law or regulation, but is generally the last day of the month for which the last payment was made in full. Figure 2 illustrates how this works:

- Jane, a QHP enrollee receiving an APTC, fails to pay the premium for April by the insurer’s due date, and she enters a grace period of three months (April, May and June). If she does not pay all outstanding premiums by the end of the grace period, her coverage can be terminated effective the last day of April.

- John, a QHP enrollee who is not receiving an APTC, fails to pay the premium for April by the insurer’s due date (for example, March 31), and then does not pay in full by the end of the grace period (April 30). His coverage can be terminated effective the last day of March (the last month for which a payment was made).

| FIGURE 2: What Happens if Premiums Are Not Paid in Full by the End of the Grace Period? |

| JANE: Receives APTCs and is eligible for a three month grace period |

|

| JOHN: Does not receive APTCs and is eligible for a one month grace period |

|

If an enrollee’s plan is terminated for non-payment, when can they re-enroll in coverage?

Once an enrollee’s plan has been terminated, they are not able to re-enroll in a marketplace QHP until the next open enrollment period, unless they qualify for a special enrollment period in the interim. Loss of coverage for failure to pay premiums does not trigger a special enrollment period.

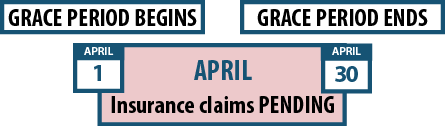

Are insurers required to pay medical claims incurred during the grace period?

Insurers must pay for medical care received during the first month of the grace period for enrollees who are receiving an APTC. However, for the second and third months of the grace period, insurers may withhold (or “pend”) payment for medical claims until the enrollee pays all outstanding premiums. If an enrollee’s coverage is terminated for failure to make all payments in full, the individual will be responsible for paying any medical expenses incurred during the second and third months of the grace period.

For enrollees not receiving an APTC, the insurance company may withhold payments during the grace period subject to any relevant state law or regulation. The enrollee may be responsible for these charges if payment is not made in full by the end of the grace period.

Insurers are supposed to let providers know if a policyholder’s claims are being held because they are in a grace period. Providers may choose not to provide care until premiums are paid, even though the person is still technically enrolled in the plan until the grace period ends.

Figure 3 shows two examples of how medical claims are treated when an individual is in a grace period:

- Jane, who is enrolled in a QHP and receives APTC, fails to make a premium payment for April by the insurer’s due date, and enters a grace period that lasts until June 30. During April (the first month of the grace period), her insurance company must cover any medical expenses she incurs. However, if she does not pay in full and remains in the grace period in May or June (months two and three of the grace period), any medical bills from services in those months will be held. If at the end of the grace period she has not yet paid in full, the insurance company will terminate her coverage effective the last day of April and she will be responsible for paying all medical bills incurred during May and June.

- John is enrolled in a QHP but does not receive APTC. He fails to make a premium payment for April by the insurer’s due date and enters a 30 day grace period. While he is in the 30 day grace period, any medical bills from services he receives will be held by the insurance company. If he fails to make all outstanding amounts owed in full by the end of the grace period, his insurer can terminate his coverage and he will be responsible for paying these bills.

| FIGURE 3: Medical Claim Payments During Grace Periods |

| JANE: Receives APTCs and is eligible for a three month grace period |

If payments are not made in full by the end of the grace period and Jane’s coverage is retroactively terminated to the last day of April, she will be responsible for paying any pended claims after that date. |

| JOHN: Does not receive APTCs and is eligible for a one month grace period |

If payments are not made in full by the end of the grace period and John’s coverage is retroactively terminated to the last day of March, he will be responsible for paying any pended claims after that date. |

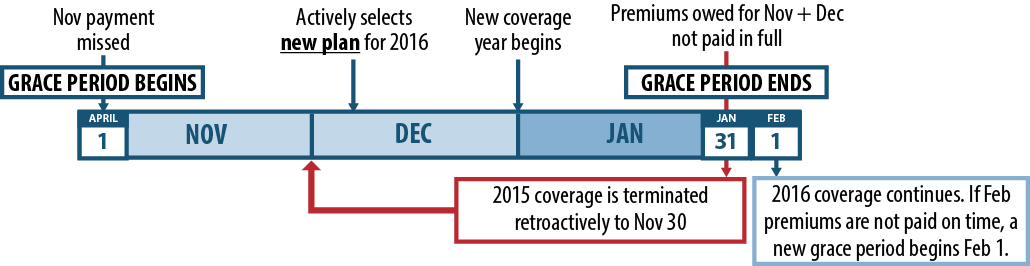

What happens when the grace period spans two coverage years?

In some cases, an individual receiving an APTC may have a grace period that spans two plan years. For example, a person who fails to pay their November premium will get a grace period that extends for three months until the end of January of the following year (overlapping with the next open enrollment period and coverage year). If the enrollee is auto-enrolled or actively selects a new plan for the next coverage year during the open enrollment period, the insurer must accept the enrollment.

If the enrollee does not pay all premiums by the end of the grace period but is auto-enrolled into or actively selects the same plan, the insurer can terminate the coverage retroactively to the last day of the first month of the grace period. This is true even if the enrollee pays a premium for the new coverage year (for example, for January) because the insurer can apply this payment to any past due amounts owed for the months of grace period.

If the enrollee is in a grace period during open enrollment and actively selects a different plan from the same insurer or a plan from another insurer, the enrollee’s coverage for the new plan year cannot be terminated when the grace period expires. Additionally, any payments made for the new coverage year cannot be applied to any prior outstanding amounts.[1]

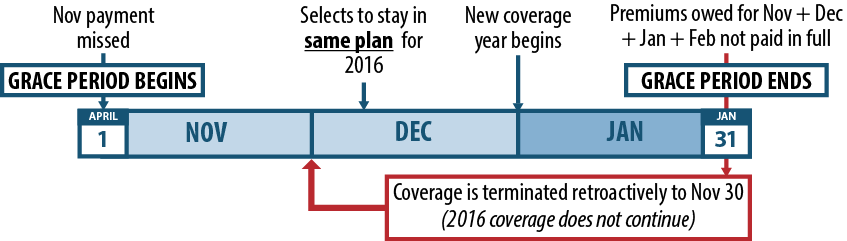

Figure 4 shows two examples of what happens when a grace period spans two coverage years:

- John is enrolled in a QHP and receives APTC. He fails to pay his November premium, and enters a grace period that lasts until the end of January. During open enrollment in December, John actively selects the same plan (or does nothing and is auto-enrolled in the same plan) and pays a premium for January. The insurer can apply this payment for the outstanding amount owed for November. At the end of January, if John has not submitted payment for both December and January, his coverage will be terminated as of November 30 (the last day of the first month of the grace period).

- Under the same circumstance, if John instead actively selects a different plan from the same insurer (or a plan from a different insurer), John’s payment for January would be credited for this new coverage year. If he does not pay the premiums owed from November and December by the end of the grace period for his prior year’s coverage (i.e. the end of January), his coverage for the prior year would be retroactively terminated to the last day of November, but his coverage for the new calendar year would not be terminated.

| FIGURE 4: Grace Periods Spanning Coverage Years |

| John is Auto-Enrolled or Actively Selects the Same Plan for the Following Coverage Year |

If John pays his January premium for the new coverage year, the insurer is allowed to apply this payment for the outstanding amount owed for November. |

| John Actively Selects a New Plan for the Following Coverage Year (with same insurer or with different insurer) |

If John pays his January premium for the new coverage year, the insurer is NOT allowed to apply this payment for the outstanding amount owed for November. |

What happens if a premium payment is below the full amount owed?

Some states have policies regarding a premium payment threshold, which is a minimum amount or percentage of the full premium that, if paid, should be considered paid in full. This is done so that accidental underpayments by small amounts do not trigger a grace period for enrollees.

States may set a particular standard in state law or regulation. For example, a state can set a $5 threshold of the total amount owed. This would mean that if an enrollee sends in payment that is within $5 of what is owed, they will not be considered behind in payments and no grace period can be triggered.

Unless otherwise indicated in state law, insurers in states served by the FFM have the option of adopting a premium payment threshold policy. The FFM recommends a threshold of 95 percent of the premium or higher, which means that if an enrollee sends in at least 95 percent of what is owed, they will not be considered past-due. Some insurers may consider the first month’s premium to be paid in full as long as it is above their designated payment threshold.

If an enrollee continues to underpay over the course of several months and the accumulated underpayment amount exceeds the allowable threshold, they can be treated as if they have failed to make a payment and put in a grace period. For example, if an enrollee’s plan has an allowable threshold of $5 and a premium of $101, but they send in $100 each month, by the sixth month, they will have accumulated $6 in underpayments, which exceeds the $5 threshold. It is important to note that once an enrollee is in a grace period, the premium payment threshold no longer applies and the enrollee must make all past-due payments in full to ensure that her coverage continues.

Can a person be denied coverage if they have previously had their coverage terminated because of unpaid premiums?

Beginning in plan year 2023, insurers in all states cannot deny coverage to a person whose coverage was terminated in a previous year due to unpaid premiums. Additionally, insurers cannot require a person to pay any unpaid premiums from previous years in order to enroll in a new health plan.[2] However, if a person is in a grace period during open enrollment or a special enrollment period, and is re-enrolled into or actively enrolls in the same plan, then they will still need to pay any past-due premiums in order to maintain their coverage (see example in Figure 4).

[1] Patient Protection and Affordable Care Act, “Revised Bulletin #10 on Grace Periods Related to Terminations for Non-Payment of Premiums and Enrollment through the Federally-facilitated Marketplace across Benefit Years,” CCIIO Informational Bulletin, September 12, 2014,

[2] www.federalregister.gov/documents/2022/05/06/2022-09438/patient-protection-and-affordable-care-act-hhs-notice-of-benefit-and-payment-parameters-for-2023