Updated August 2023

Household size is a key factor in determining eligibility for the premium tax credit. The following Q&A explains the rules on household size and how it affects eligibility for and the amount of the premium tax credit.

Note that many guidelines and thresholds are indexed and change each enrollment year. For reference, please see the Yearly Income Guidelines and Thresholds Reference Guide.

Why does household size matter when calculating eligibility for the premium tax credit?

Eligibility for the premium tax credit is based on a family’s income as a percentage of the federal poverty line (FPL). The poverty line increases with household size. Table 1 shows the federal poverty guidelines for different household sizes in the 48 contiguous states and the of Columbia. (Alaska and Hawaii each have their own federal poverty guidelines.) A family’s poverty line percentage is their annual income divided by the poverty line for their household size. For example, a married couple with two children earning $45,000 a year would divide their household income by the poverty line for a family of four — $30,000 in 2023 — to calculate their income at 150 percent of the federal poverty line. This puts them in the eligible income range for a premium tax credit and cost-sharing reduction. (For more information on cost-sharing reductions, see Key Facts: Cost-Sharing Reductions.)

| TABLE 1: Federal Poverty Line Guidelines (2023 guidelines are used for the 2024 coverage year for PTC) |

|||||

| Household Size | % of Federal Poverty Line (2023 guidelines) | ||||

| 100% | 138% | 200% | 250% | 400% | |

| 1 | $14,580 | $20,120 | $29,160 | $36,450 | $58,320 |

| 2 | $19,720 | $27,214 | $39,440 | $49,300 | $78,880 |

| 3 | $24,860 | $34,307 | $49,720 | $62,150 | $99,440 |

| 4 | $30,000 | $41,400 | $60,000 | $75,000 | $120,000 |

| 5 | $35,140 | $48,493 | $70,280 | $87,850 | $140,560 |

Income as a percentage of the federal poverty line also sets the amount of premium tax credit a household is eligible to receive. Families at different income levels are expected to contribute different percentages of their income towards premiums (see Table 2), with higher income families paying a greater percentage of their income towards premiums than lower income families. The premium tax credit is determined by subtracting the premium contribution from the cost of a benchmark plan so as premium contributions rise, the premium tax credit is reduced. (For more information on how the premium tax credit is calculated, see Key Facts: The Premium Tax Credit.)

| TABLE 2: Expected Premium Contribution Based on Income (for 2024 coverage) |

|

| Annual Household Income (% of FPL) |

Expected Premium Contribution (% of income) |

| Less than 150% | 0% |

| 200% | 2% |

| 250% | 4% |

| 300% | 6% |

| 400% or more | 8.5% |

How does the marketplace establish household size to determine eligibility for the premium tax credit?

A person’s household for premium tax credit eligibility includes all the individuals on their tax return — the tax filer, the tax filer’s spouse (if married filing jointly), and any dependents. Everyone is included in the household, even family members who are not applying for coverage and those who are not eligible for a premium tax credit. For example:

- Maria and Simon are married and have one child, Elaine, whom they claim as a tax dependent. They have a tax household of three people and earn $47,000 a year (which is 189 percent of the poverty line in 2023). Elaine is eligible for the Children’s Health Insurance Program (CHIP), making her ineligible for a premium tax credit, but she’s still included in Maria and Simon’s household for determining premium tax credit eligibility.

- Suppose that Maria and Simon also have an older daughter, Cora, who is 22 and living at home with her parents. Cora just graduated from college and is working full-time. She cannot be claimed as a tax dependent by her parents and files her own taxes. Even though Cora lives with her family, she is a household of one for premium tax credit purposes because she cannot be claimed by her parents.

Who can be in a household together?

The composition of the household for premium tax credit purposes follows Internal Revenue Service (IRS) rules for filing status and dependents. For more information on tax rules, see The Health Assister’s Guide to Tax Rules.

How do you determine the household of married couples who file separate tax returns?

To be eligible for a premium tax credit, married couples must file a joint tax return. Married couples who file separate returns are not eligible for a premium tax credit, with the following exceptions:

- A married person qualifies to file as head of household. A person who is married but does not plan to file jointly with a spouse can sometimes qualify as Head of Household, a filing status that allows a person to be eligible for a premium tax credit, rather than Married Filing Separately, which does not. In general, a person can be Head of Household if they are unmarried or considered unmarried. A married person is considered unmarried if they will live apart from their spouse in the last six months of the tax year and pays more than half of the cost of keeping up the home for their dependent child.

- A married person is a survivor of domestic violence or abuse. A taxpayer who lives apart from their spouse and is unable or unwilling to file a joint tax return due to domestic violence will be deemed to satisfy the joint filing requirement by making an attestation on their tax return. Under this IRS rule, taxpayers may qualify for the premium tax credit despite having the tax filing status of married filing separately; or

- A married person has been abandoned by their spouse. A taxpayer is still eligible for a premium tax credit despite filing separately if they have been abandoned by a spouse and certify on their tax return that the spouse cannot be located after using “reasonable diligence.”

The household of a person who qualifies for one of these exceptions includes the person and anyone they claim as a dependent on the tax return.

Note also that married people who file as Head of Household are always eligible for a premium tax credit, but married people who are survivors of domestic abuse or have been abandoned by their spouse can qualify for those exceptions for no more than three consecutive years. (For more information on these exceptions, see the IRS rules.)

Do family members have to enroll in the same plan to be included in the same premium tax credit?

The tax household for premium credit eligibility is based on tax rules and doesn’t always align with insurers’ rules about who can enroll in the same plan. In the marketplace, people have the option to purchase individual or family policies. Typically, health insurers limit family plans to only immediate family members (e.g., parents and their children). That means that a member of a tax household may need to enroll in a separate plan if they aren’t the child of the taxpayer, even if they’re properly claimed as a dependent and part of the household for premium tax credit purposes. For example:

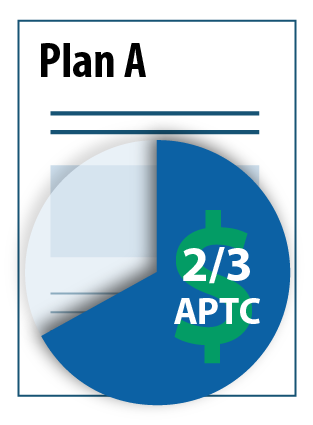

- Serena lives with her son, Jacob, and her aunt, Martha, who Serena supports. Serena is a tax filer and claims both Jacob and Martha as tax dependents. Because most insurers wouldn’t include Martha in a family plan covering Serena and Jacob, Martha will be in a separate health plan. However, even though they are covered through separate health plans, the family is still one tax unit, so their premium tax credit is determined as a household of three, and the advance payment of the premium tax credit (APTC) is applied proportionally to the two plans (see Figure 1).

- Even though part of the advance payment goes to Martha’s health insurer during the year, Serena will claim the tax credit and be responsible for reconciling the entire household’s APTC, including Martha’s portion. Because Martha is a tax dependent, not a tax filer, she cannot directly claim the premium tax credit.

| FIGURE 1: Example Allocation of APTC If Multiple Plans Cover One Household |

|

| Household of 3 (SERENA, JACOB, MARTHA) | |

Plan A Enrollees: SERENA and JACOB |

Plan B Enrollees: MARTHA |

Can family members in different tax households enroll in the same plan?

Taxpayers’ children under age 26 may enroll in their parents’ plan, even if they are not dependents and have a separate tax household. However, HealthCare.gov does not currently allow households with multiple independent tax filers on separate tax returns (e.g. a non-dependent child and their parent(s)) to apply for or enroll in coverage with financial assistance together.

In states that use HealthCare.gov, independent tax filers who would like to be considered for financial assistance should submit a separate marketplace application from other tax filers in their immediate family. Alternatively, families in this situation can submit an application that does not request financial assistance for anyone, enroll in a plan together, pay the full premium for the coverage, and then claim the premium tax credit when they file taxes (if eligible).

Families comprised of multiple tax households who live in states that do not use HealthCare.gov should contact their state marketplace for instructions on applying for coverage and financial help.

How do mid-year changes in a person’s household affect premium tax credit eligibility?

A change in household size affects the household income level as a percentage of the poverty line, changing the premium tax credit the taxpayer is eligible to receive. Since the premium tax credit is based on annual income, the change in household size affects the premium tax credit amount for the entire year, not just for the months after the change occurs. For example:

- A married couple with a projected income of $39,440 has an income at 200 percent of the poverty line. If they have a baby sometime during the year, they would become a household of three, and their income would be 159 percent of the poverty line. This change in poverty level income will lower the household’s expected contribution from 2 percent to 0.36 percent of income, which will make them eligible for a larger credit.

To ensure that individuals receive the correct APTC amount for the year, household size and other changes should be immediately reported to the marketplace.

Are premium tax credit and Medicaid households the same?

No. For the premium tax credit, members of a tax household are always in the same household when determining their eligibility. For Medicaid, household size and composition are determined separately for each member of the household. The rules look at more than just tax filing status; familial relationships and who physically lives in a household are also part of the determination. In some cases, Medicaid follows the premium tax household rules, but in some cases it will not.

In addition, household rules for the premium tax credit are uniform across all states, but Medicaid provides some state options — such as some flexibility in the age limits for the definition of a child — that result in variability in household size depending on the state. For more information on the Medicaid household rules, see Key Facts: Determining Household Size for Medicaid.

How will the marketplace determine whether to use Medicaid or premium tax credit household rules to determine eligibility?

An applicant can’t be eligible for a premium tax credit if they are eligible for Medicaid, so the marketplace applies the state Medicaid rules first. It determines the family size of each individual in the tax household using Medicaid rules. (If the individual is assessed or determined eligible for Medicaid, they will be transferred to their state’s Medicaid agency.) If the individual is ineligible for Medicaid, then the marketplace will look at their household and eligibility for the premium tax credit using premium tax credit rules.

—

For updated yearly percentages, please see Reference Guide: Yearly Guidelines and Thresholds.