Updated August 2023

Financial eligibility for the premium tax credit, most categories of Medicaid, and the Children’s Health Insurance Program (CHIP) is determined using a tax-based measure of income called modified adjusted gross income (MAGI). The following Q&A explains what income is included in MAGI.

Note that many guidelines and thresholds are indexed and change each enrollment year. For reference, please see the Yearly Income Guidelines and Thresholds Reference Guide.

How do ACA marketplaces, Medicaid, and CHIP measure a person’s income?

For the premium tax credit, most categories of Medicaid eligibility, and CHIP, all ACA marketplaces and state Medicaid and CHIP agencies determine a household’s income using MAGI. States’ previous rules for counting income continue to apply to people who qualify for Medicaid based on age or disability or because they are children in foster care.

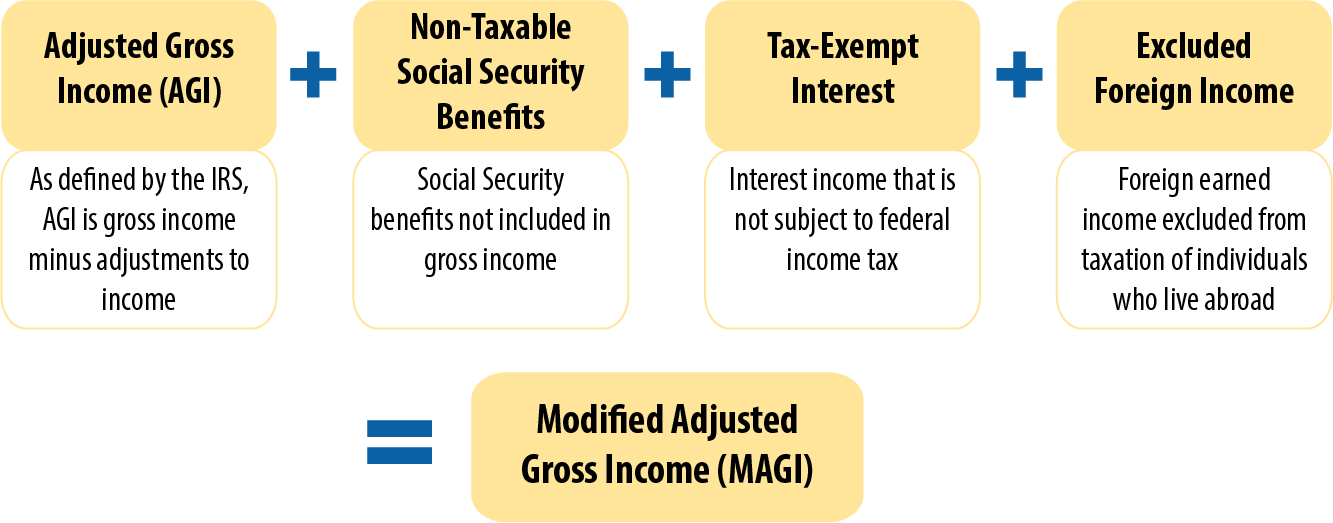

MAGI is adjusted gross income (AGI) plus tax-exempt interest, Social Security benefits not included in gross income, and excluded foreign income. Each of these items has a specific tax definition; in most cases they can be located on an individual’s tax return (see Figure 1). (In addition, Medicaid does not count certain Native American and Alaska Native income in MAGI.)

| FIGURE 1: Formula for Calculating Modified Adjusted Gross Income |

|

What is adjusted gross income?

Adjusted gross income is the difference between an individual’s gross income (that is, income from any source that is not exempt from tax) and deductions for certain expenses. These deductions are referred to as “adjustments to income” or “above the line” deductions. Common deductions include certain contributions to an individual retirement account (IRA) or health savings account (HSA) and payment of student loan interest. Many income adjustments are capped or phased out based on income. IRS Publication 17 explains adjustments to income in more detail.

What types of income count towards MAGI?

All income is taxable unless it’s specifically exempted by law. Income does not only refer to cash wages. It can come in the form of money, property, or services that a person receives.

Table 1 provides examples of taxable and non-taxable income. IRS Publication 525 has a detailed discussion of many kinds of income and explains whether they are subject to taxation.

| TABLE 1: Examples of Taxable Income and Non-Taxable Income (see IRS Publication 525 for details and exceptions) |

|

| Examples of Taxable Income | |

| Wages, salaries, bonuses, commissions | IRA distributions |

| Annuities | Jury duty fees |

| Awards | Military pay |

| Back pay | Military pensions |

| Breach of contract | Notary fees |

| Business income/Self-employment income | Partnership, estate, and S-corporation income |

| Compensation for personal services | Pensions |

| Debts forgiven | Prizes |

| Director’s fees | Punitive damages |

| Disability benefits (employer-funded) | Unemployment compensation |

| Discounts | Railroad retirement—Tier I (portion may be taxable) |

| Dividends | Railroad retirement—Tier II |

| Employee awards | Refund of state taxes* |

| Employee bonuses | Rents (gross rent) |

| Estate and trust income | Rewards |

| Farm income | Royalties |

| Fees | Severance pay |

| Gains from sale of property or securities | Self-employment |

| Gambling winnings | Non-employee compensation |

| Hobby income | Social Security benefits (portion may be taxable) |

| Interest | Supplemental unemployment benefits |

| Interest on life insurance dividends | Taxable scholarships and grants |

| Tips and gratuities | |

| Examples of Non-Taxable Income | |

| Aid to Families with Dependent Children (AFDC) | Meals and lodging for the employer’s convenience |

| Child support received | Payments to the beneficiary of a deceased employee |

| Damages for physical injury (other than punitive) | Payments in lieu of worker’s compensation |

| Death payments | Relocation payments |

| Dividends on life insurance | Rental allowance of clergyman |

| Federal Employees’ Compensation Act payments | Sickness and injury payments |

| Federal income tax refunds | Social Security benefits (portion may be taxable) |

| Gifts | Supplemental Security Income (SSI) |

| Inheritance or bequest | Temporary Assistance for Needy Families (TANF) |

| Insurance proceeds (accident, casualty, health, life) | Veterans’ benefits |

| Interest on tax-free securities | Welfare payments (including TANF) and food stamps |

| Interest on EE/I bonds redeemed for qualified higher education expenses | Workers’ compensation and similar payments |

*State tax credits and offsets are included as taxable income if the filer claimed an itemized deduction for state taxes that was later refunded.

Is income subtracted from workers’ paychecks as a pre-tax deduction counted in MAGI?

No. Pre-tax deductions — such as health insurance premiums, retirement plan contributions, or flexible spending accounts — are taken out of wages by the employer. Since this income isn’t taxed, it doesn’t count towards a household’s MAGI. The wages in Box 1 of Form W-2 already exclude any pre-tax benefits so they don’t appear on the tax return as income or deductions.Does MAGI count any income sources that are not taxed?

Yes. Some forms of income that are non-taxable or only partially taxable are included in MAGI and affect financial eligibility for premium tax credits and Medicaid. Specifically:- Tax-exempt interest. Interest on certain types of investments is not subject to federal income tax but is included in MAGI. These investments include many state and municipal bonds, as well as exempt-interest dividends from mutual fund distributions.

- Non-taxable Social Security benefits. For many people, particularly those with no other source of income, Social Security benefits are not taxed at all. However, if there is other income, a portion of the benefit might be taxed. Social Security benefits are reported on Form SSA-1099 (the Social Security Benefit Statement) and, whether or not those benefits are taxable, the full amount is included in MAGI.

- Foreign income. Under section 911 of the Internal Revenue Code, U.S. citizens and resident aliens living outside the U.S. can exclude some earned income for tax purposes if they meet certain residency or physical presence tests. Any foreign income excluded under this section must be added back when calculating MAGI.

Whose income is included in household income?

Household income is the MAGI of the tax filer and spouse, plus the MAGI of any dependent who is required to file a tax return. A dependent’s income is only included if they are required to file taxes; if they file taxes for another reason but had no legal filing requirement, their income is not included.Is a tax dependent’s income ever included in household income?

If a dependent has a tax filing requirement, their MAGI is included in household income. A dependent must file a tax return for 2023 if they received at least $13,850 in earned income; $1,250 in unearned income; or if the earned and unearned income together totals more than the greater of $1,250 or earned income (up to $13,450) plus $400. In general, unearned income is defined as investment income; Supplemental Security Income (SSI) and Social Security benefits are not counted in determining whether a dependent has a tax-filing requirement. However, if the dependent does have a tax filing requirement, the dependent’s Social Security benefits will be counted toward the household’s MAGI. If a dependent does not have a filing requirement but files anyway — for example, to get a refund of taxes withheld from their paycheck — the dependent’s income would not be included in household income.What time frame is used to determine household income?

Financial eligibility for the premium tax credit and Medicaid is based on income for a specified “budget period.” For the premium tax credit, the budget period is the calendar year during which the advance premium tax credit is received. When determining eligibility for an advance premium tax credit, the applicant projects their household income for the entire calendar year. Medicaid eligibility, however, is usually based on current monthly income. But for people with income that varies over the year, states must consider yearly income if the person wouldn’t be eligible based on monthly income. For example, a seasonal worker might be over the income limit based on monthly income if they are employed when they apply but would be under the limit if their yearly income (including the months where they are unemployed) is considered. The Medicaid agency must determine eligibility using the yearly income. This prevents situations where people are considered ineligible for the ACA marketplace based on their yearly income and ineligible for Medicaid based on their monthly income. In addition, Medicaid also treats some lump-sum income differently than the ACA marketplace, by considering it only in the month received.How does MAGI differ from Medicaid’s former rules for counting household income?

The MAGI methodology for calculating income differs significantly from previous Medicaid rules. Some income that Medicaid used to consider part of household income is no longer counted, such as child support received, veterans’ benefits, workers’ compensation, gifts and inheritances, and Temporary Assistance for Needy Families (TANF) and SSI payments. Table 2 summarizes the differences between the former Medicaid rules and the current MAGI rules. In addition, states can no longer impose asset or resource limits, and various income disregards have been replaced by a standard disregard equal to 5 percent of the poverty line. There are also differences in who is included in a household and, therefore, whose income is counted.| TABLE 2: Differences in Counting Income Sources Between Former Medicaid Rules and MAGI Medicaid Rules | ||

| Income Source | Former Medicaid Rules | MAGI Medicaid Rules |

| Self-employment income | Counted with deductions for some, but not all, business expenses | Counted with deductions for most expenses, depreciation, and business losses |

| Salary deferrals (flexible spending, cafeteria, and 401(k) plans) | Counted | Not counted |

| Child support received | Counted | Not counted |

| Alimony paid | Not deducted from income | Deducted from income (subject to new rules in 2019) |

| Veterans’ benefits | Counted | Not counted |

| Workers’ compensation | Counted | Not counted |

| Gifts and inheritances | Counted as lump sum income in month received | Not counted |

| TANF & SSI | Counted | Not counted |